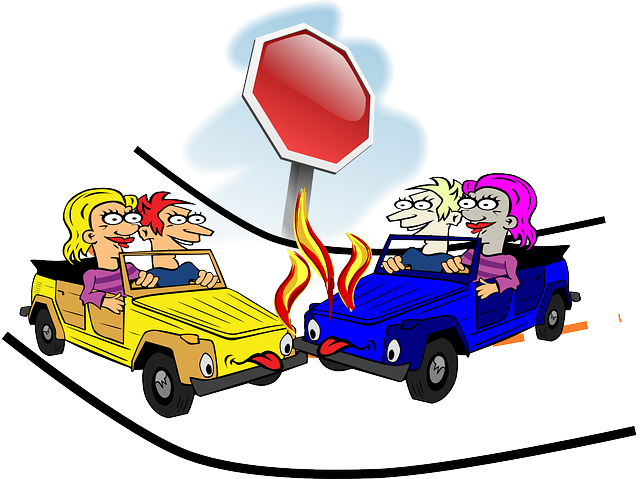

Collision coverage is a crucial component of auto insurance, protecting drivers from financial burdens after accidents by covering repair or replacement costs up to policy limits. It specifically mitigates damages caused by collisions, with options including Collision and Comprehensive Coverage. Policies vary based on driver history, vehicle type, location, and deductibles, impacting premiums. Understanding collision coverage, its exclusions, and the claims process is vital for drivers to make informed decisions, ensuring peace of mind on the road and financial protection in case of accidents.

In the event of a car accident, collision insurance plays a pivotal role in mitigating financial losses. This comprehensive guide delves into the intricacies of collision coverage, exploring what it entails and how it safeguards your investment. From understanding policy specifics to navigating claims processes, we demystify this essential aspect of auto insurance. Discover the various types of collision protection available, common exclusions, and factors influencing premiums. Learn why collision insurance is crucial and how it compares to other policies, offering valuable tips for selecting the optimal coverage for peace of mind on the road.

Understanding Collision Insurance: What It Covers

Collision insurance, also known as collision coverage, is a crucial component of auto insurance policies designed to protect drivers from financial burdens resulting from car accidents. It offers comprehensive protection against the cost of repairing or replacing your vehicle after a collision, regardless of who is at fault. This includes damage to both your car and any other vehicles involved in the accident.

When you have collision coverage, your insurance provider will step in and cover the repair or replacement expenses up to the value of your policy. This ensures that you don’t have to bear the financial brunt of unexpected collisions. Collision coverage is particularly valuable for drivers who own expensive vehicles or those who frequently drive in areas with high traffic congestion or known for road accidents.

Types of Collision Coverage Available

When it comes to collision insurance, there are several types of coverage options available to drivers, each designed to cater to different needs and preferences. The most common forms include Collision Coverage for direct damage resulting from a crash with another vehicle or object. This type of insurance covers repairs or replacement costs, offering peace of mind knowing your financial obligations are mitigated in case of an accident.

Additionally, Comprehensive Coverage is another option, which protects against incidents beyond collisions, such as theft, vandalism, natural disasters, and animal-related damages. While it’s not strictly collision-focused, comprehensive insurance provides broader protection for various unforeseen events that could affect your vehicle. Understanding these coverage types allows drivers to make informed decisions when selecting their ideal insurance plan.

How Collision Insurance Works After an Accident

After a car accident, Collision Coverage steps in to help with repairs or replacement costs. This type of insurance is designed to pay for damages when your vehicle collides with another object, whether it’s another vehicle, a fixed structure, or even a pedestrian. When an accident occurs, you file a claim with your insurance provider, who will assess the damage and determine the cost of repairs.

Collision Coverage typically covers the cost of repairing or replacing your vehicle up to its actual cash value (ACV). This means if your car is deemed a total loss, the insurance company will pay out the ACV, minus your deductible. Understanding the terms and conditions of your policy is essential to knowing what’s covered and how much you’ll be responsible for after an accident.

Common Exclusions in Collision Policy

Collision insurance policies typically cover repairs or replacements for your vehicle after a collision, providing financial protection against unexpected costs. However, it’s important to be aware that these policies often come with certain exclusions. Common exclusions include damage caused by wear and tear, normal maintenance, or events not involving another vehicle, such as animal encounters or natural disasters.

Some policies may also exclude specific types of accidents, like those resulting from driving under the influence, racing, or willful destruction. Additionally, the level of collision coverage can vary greatly between providers, so it’s crucial to read the policy details carefully to understand what’s covered and what isn’t. This ensures you’re adequately protected in the event of a car accident.

Factors Affecting Collision Insurance Premiums

Several factors influence collision insurance premiums, and understanding these can help drivers make informed decisions when purchasing a policy. One of the primary considerations is the driver’s record. A clean driving history with no previous accidents or violations typically results in lower rates. Conversely, a history of fender benders, moving violations, or severe at-fault accidents will increase premium costs significantly. The type and age of the vehicle are also critical; newer cars generally have higher insurance costs due to their more expensive repairs and replacement parts.

Additionally, where you live plays a substantial role in your collision coverage premiums. Areas with higher population densities, frequent traffic congestion, or risky weather conditions often lead to more accidents, prompting insurers to charge higher rates to compensate for the increased risk. The cost of collision insurance can also vary based on the chosen deductibles; selecting a higher deductible may reduce premiums but requires the policyholder to pay more out-of-pocket in case of an accident.

Comparison with Other Auto Insurance Policies

Collision insurance is a specific type of auto insurance coverage that sets it apart from other standard policies. While comprehensive and liability insurances offer broad protection against various risks, collision coverage focuses exclusively on damage to your vehicle resulting from accidents. This targeted approach makes collision coverage a vital component for drivers who want to safeguard their investment in their vehicles.

In comparison, comprehensive insurance protects against non-accident-related damages like theft, vandalism, or natural disasters, while liability insurance covers the costs of damaged property and medical expenses for injured parties in an accident. Collision coverage, on the other hand, kicks in when your car sustains damage due to a collision with another vehicle or object, providing financial assistance for repairs or, if necessary, total vehicle replacement.

Claims Process and Procedure for Collision Insurance

When a car accident occurs, understanding the collision insurance claims process is crucial for policyholders. The first step involves notifying your insurance provider as soon as possible after the incident. This can be done by calling or visiting their website to report the claim. You’ll need to provide details about the accident, including dates, times, and locations, along with a description of what happened. Collision coverage is designed to protect you in such scenarios, ensuring that repairs or replacement costs are covered up to the limits specified in your policy.

After reporting the claim, the insurance company will assign an adjuster who will gather information from all parties involved. They will inspect the damaged vehicle and review relevant documents, including police reports and medical records if necessary. The adjuster will then provide a settlement offer based on the repair estimates and the policy terms. It’s important to review this offer carefully and communicate any concerns or questions with your insurance representative to ensure a fair process.

Legal Implications of Not Having Collision Coverage

Not having collision coverage on your auto insurance policy can have significant legal implications, especially in the event of a car accident. When you’re involved in a crash, the other driver’s liability insurance step in to cover damages if they’re at fault. However, if you don’t have collision coverage, you’re personally responsible for paying for any repairs or losses to your vehicle, which can lead to substantial financial burdens.

In many jurisdictions, driving without collision coverage may also result in legal penalties and fines. Moreover, if the other driver doesn’t have enough liability insurance to cover all the damages, your personal assets could be at risk. Collision coverage acts as a safety net by protecting you from these potential hardships, ensuring that repairs or replacements are covered regardless of fault.

Tips for Opting for the Best Collision Insurance Plan

When opting for a collision insurance plan, it’s crucial to consider several factors to ensure comprehensive protection. Firstly, evaluate your vehicle’s make and model; some older or high-end vehicles might require specialized coverage due to their value and repair costs. Secondly, assess your driving history; if you’re a safe driver with no major accidents, you may qualify for discounted rates.

Additionally, compare different insurance providers and their collision coverage policies. Look into the types of damages covered, deductibles, and whether they offer optional add-ons like rental car coverage or roadside assistance. Remember to read the policy details carefully, understanding what’s excluded and included to make an informed decision that aligns with your needs.